|

|

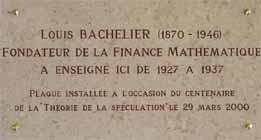

The First Bachelier Colloquium

Besançon, March 2000.

The colloquium was organized on occasion of the centenary of the

Bachelier thesis "Théorie de la spéculation", the work which is

the foundation stone of the modern financial mathematics

and theory of stochastic processes.

The scientific and cultural programs were highly appreciated by

the participants. The colloquium was accompanied by a series of

manifestations including opening a commemorative plate on the wall

of the university building where Bachelier, the founding father of

stochastic calculus and mathematical finance, gave his lectures.

A street in Besançon was named after Bachelier.

|

The Pro o o |

|

|

The Second Bachelier Colloquium

Métabief, France, on January 9-15, 2005.

The meeting was dedicated to the outstanding mathematician, member of Russian Academy of Sciences, professor Albert Shiryaev, on the occasion of his 70th anniversary. He was the honorary guest of the meeting and gave a lecture course on optimal stopping problem.

The Proceedings of the 2nd Colloquium :

From Stochastic Calculus to Mathematical Finance.

The Shiryaev Festschrift. Springer-Verlag, 2006, 634 pp.

Eds: Kabanov Yu., Liptser R., Stoyanov J.

|

|

|

| |

The Third Bachelier Colloquium

Métabief, France, on January 6-13, 2008.

The main topics of the colloquium were: financial markets

with transaction costs, dynamic risk measures, BSDEs in financial

problems, econometric approach to bank ratings, utility theory.

|

|

The Fourth Bachelier Colloquium

Métabief, France, on January 6-13, 2010.

The main topics of the colloquium were: financial markets

with transaction costs, mathematics of financial crisis, BSDEs in financial

problems, duality methods, stochastic control, optimal stopping.

|

|

The Fifth Bachelier Colloquium

Métabief, France, January 16-23, 2011.

The meeting was dedicated to our colleague Marek Musiela for his great contributions to the development of mathematical finance, on the occasion of his 60th anniversary.

The main topics of the colloquium:

financial markets

with transaction costs, mathematics of financial crisis, BSDEs in financial

problems, duality methods, stochastic control, optimal stopping.

- program 2011

|

|

The Sixth Bachelier Colloquium

Métabief, France, January 15-22, 2012.

The main topics of the colloquium: actuarial and financial models.

|

|

The Seventh Bachelier Colloquium

Métabief, France, January 13-20, 2013.

The main topics of the colloquium:

role of information in risky investments, markets with transaction costs, market microstructure,

benchmark approach, high speed trading, market viability, equilibrium models, fractional Brownian motion, defaultable securities.

|

|

|

|

The Eighth Bachelier Colloquium

Métabief, France, on January 12-28, 2014.

The main topic of the colloquium was formulated as: New trends in mathematical finance.

The Ninth Bachelier Colloquium

Métabief, France, on January 11-18, 2015.

The main topic of the colloquium was formulated as: Challenging problems in quantitative finance.

The Tenth Bachelier Colloquium

Métabief, France, on January 18-23, 2016.

Topics: arbitrage theory, stochastic control with financial applications,

information in risky investments, markets with transaction costs, market microstructure,

benchmark approach, high speed trading, equilibrium models, fractional Brownian motion, defaultable securities, optimal stopping, martingale transport, financial regulations.

The Eleventh Bachelier Colloquium

Métabief, France, on January 16-21, 2017.

Topics: arbitrage theory, markets with transaction costs, market microstructure, high speed trading, financial regulations, actuarial models, systemic risk, defaultable securities, optimal stopping, stochastic control, fractional Brownian motion, classical and non-commutative stochastic calculus.

The Twelfth Bachelier Colloquium

Métabief, France, on January 15-20, 2018.

Topics: arbitrage theory, markets with transaction costs, market microstructure, high speed trading, financial regulations, actuarial models, systemic risk, defaultable securities, optimal stopping, stochastic control, fractional Brownian motion, classical and non-commutative stochastic calculus.

The Thirteenth Bachelier Colloquium

Métabief, France, on January 7-12, 2019.

Topics: arbitrage theory, robust models, martingale transport, markets with transaction costs, energy markets, market microstructure, high speed trading, set-valued methods, actuarial models, systemic risk, defaultable securities, optimal stopping, stochastic control, fractional Brownian motion, BSDEs, classical and non-commutative stochastic calculus.

|

|

|

|

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)